Fixed Income Market Reaction

With concern about the impact to economic activity of the COVID-19 virus being blamed for the recent volatility in equities, we are also seeing an impact on the cost of trading liquid, investment grade corporate and municipal bonds. The BondWave Benchmark Data and Trading Indices includes two corporate bond and two municipal bond bid-offer spread indices. The BondWave Bid-Offer Spread Service (BOSS) measures the width of the bid-offer spread in the dealer-to-dealer market for A and BBB rated corporate bonds as well as the bid-offer spread in the dealer-to-dealer market for AA and A municipal bonds.

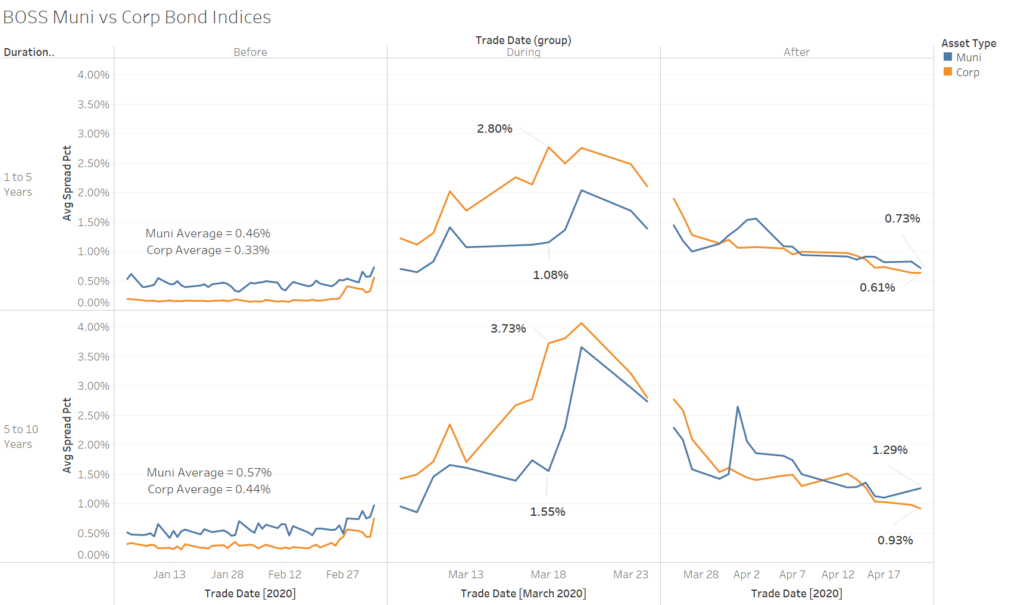

Liquidity Cost for Corporates Below Municipals for the First Time in Over a Month

The historic relationship between the bid-ask spread of corporate bonds and municipal bonds has been restored this week. Dating back to at least 2016 (when the BOSS indices began) municipal bond bid-ask spreads have been wider than corporate bond bid-ask spreads. This reflects the relative liquidity of the two bond types. However, during the height of the COVID-19 pandemic this relationship inverted.

Source: BondWave BDTI

From January 2nd to March 9th this year (‘Before’ in the above graph) the average daily difference between bid-ask spreads on municipal bonds and corporate bonds with 1 to 5 years duration was 13 basis point (46 bps vs 33 bps). For bonds with 5 to 10 years duration the difference was also 13 basis points (57 bps vs 44 bps). On March 18th the difference was -172 basis points (108 bps vs 280 bps) for 1 to 5 years duration and -218 basis points (155 bps vs 373 bps) for 5 to 10 years duration. For the past week, municipal bid-ask spreads were back to a premium over corporate bid-ask spreads. On April 21st the premium stood at 12 basis points (73 bps vs 61 bps) for 1 to 5 years duration and 36 basis points (129 bps vs 93 bps) for 5 to 10 years maturity.